Loan Reduction for Less Than Full-Time Students

The One Big Beautiful Act, or OB3, passed in July 2025 contained new provisions which will reduce the annual loan limits for students enrolled less than full-time. Full-time enrollment for most URochester programs is defined as a minimum of 12 degree-seeking credits per semester for undergraduate students, and a minimum of 9 degree-seeking credits per semester for graduate and professional students. These provisions will take effect as of July 1, 2026 for the 2026-2027 academic year. Please read on for additional information and examples of how these reductions may be applied to federal loan eligibility.

These provisions apply to all Federal Direct Subsidized, Unsubsidized, and Graduate PLUS Loans. Parent PLUS Loans will not be impacted.

Students with questions about how their enrollment status may impact their eligibility are encouraged to contact their financial aid counselor. Students and families can read more about additional federal loan changes beginning with the 2026-2027 academic year here.

General Principles of Loan Reduction

- Federal direct loan reductions will be applied to all students who are enrolled less than full-time over the course of an academic year.

- The reduction will be directly proportional to the student’s enrollment status compared to full-time status.

- All federal Direct Subsidized, Unsubsidized, and Graduate PLUS Loans are subject to reductions based on enrollment status.

- For most undergraduate programs, full-time status is defined as taking at least 12 degree-required credits in a given semester, equating to at least 24 degree-required credits over the course of an academic year.

- For most graduate programs, full-time status is defined as taking at least 9 degree-required credits in a given semester, equating to at least 18 degree-required credits over the course of an academic year.

- For graduate students in the Simon School of Business, full-time status is defined as taking at least 10.5 degree-required credits in a given semester, equating to at least 21 degree-required credits over the course of an academic year.

- While a summer semester is not required for most programs, enrollment in the summer semester will count toward a student’s total academic year enrollment for the purposes of these reductions.

Examples of Loan Reduction

Please review the examples below for a sense of how enrollment status over the course of a year can impact direct loan eligibility.

Example 1:

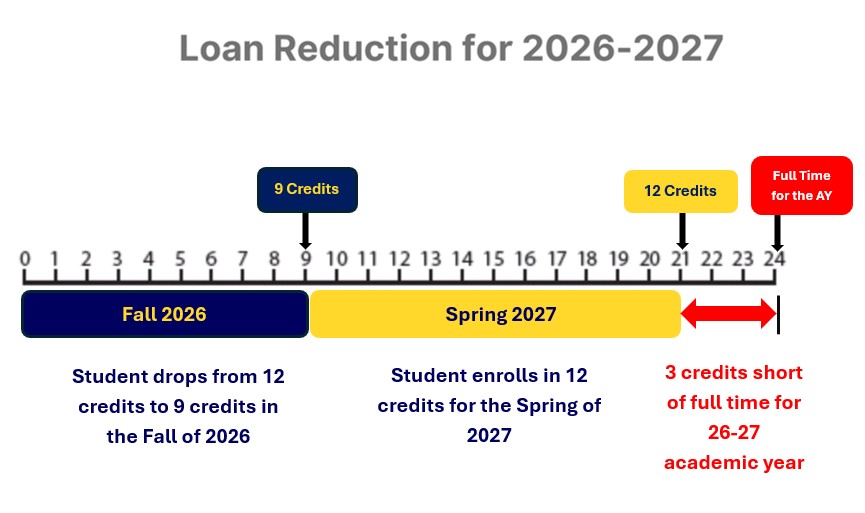

An undergraduate student drops from 12 credits in the fall semester to 9 credits. They will be enrolled in 12 credits for the spring semester.

Total Academic Year Credits for Undergraduate Full-Time Status: 24 credits

This student’s direct loan eligibility will be reduced based on prorated enrollment in 21 credits over 24 credits for full-time status.

21/24=0.875

This student’s direct loan eligibility will be reduced to 0.875 of the academic year maximum for full-time students. A Direct Subsidized Loan of $5,500 would be reduced to $4,813 ($5,500 * 0.875) after proration.

Example #2:

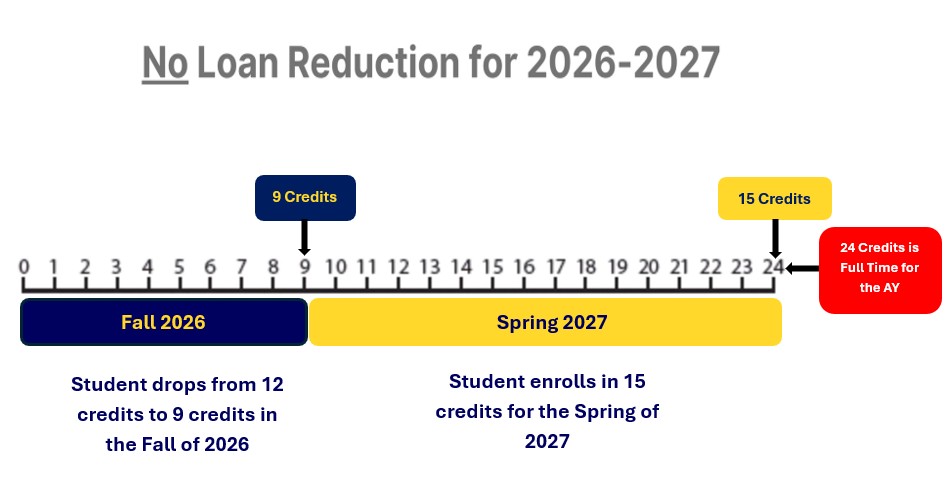

An undergraduate student is enrolled in 9 credits in the fall semester and 15 credits in the spring semester.

Student’s Total Academic Year Enrollment: 24 credits (9+15)

Total Academic Year Credits for Undergraduate Full-Time Status: 24 credits

This student’s direct loan eligibility will not be reduced as their enrollment for the academic year meets or exceeds the definition of full-time, even though their fall semester enrollment is below full-time.

Example #3:

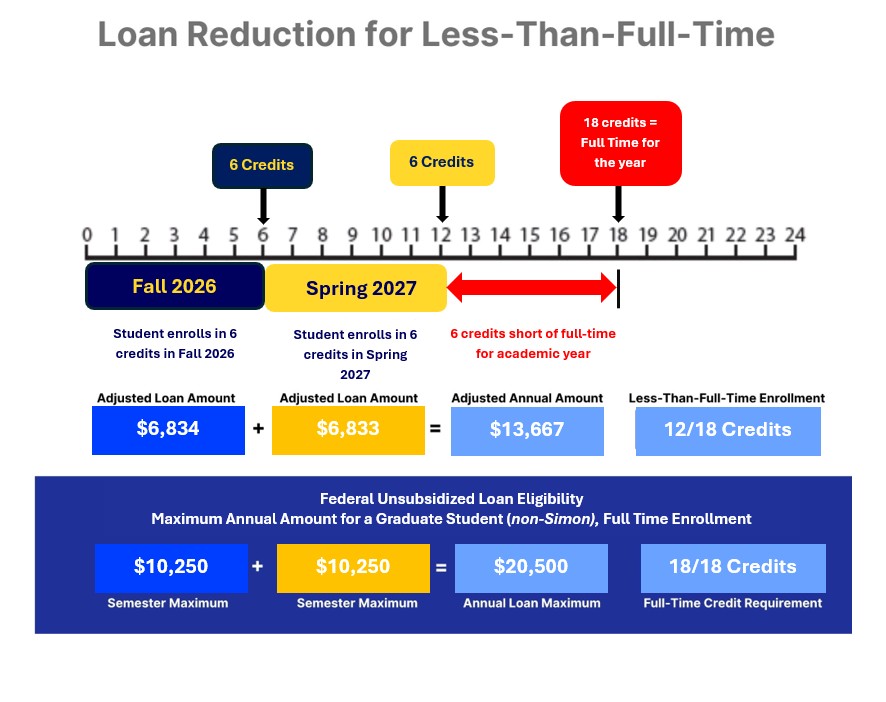

A graduate student is enrolled in 6 credits for fall and spring semesters each.

Total Academic Year Credits Graduate (non-Simon School of Business) Full-Time Status: 18 credits

This student’s direct loan eligibility would be reduced based on prorated enrollment in 12 credits over 18 credits for full-time status.

12/18=0.667

This student’s direct loan eligibility will be reduced to 0.667 of the academic year maximum for full-time students. A Direct Unsubsidized Loan of $20,500 would be reduced to $13,667 ($20,500 * 0.667) after proration.